Let us be real for a second, partner. Creating a monthly budget sounds about as fun as a root canal until you actually try to do it. We have all been there: you sit down on the 1st of the month, feeling like a financial superhero, only to find yourself “treating yourself” to a $15 artisan latte by the 10th and completely abandoning the plan by the 15th. Knowing How to Create a Monthly Budget to matters a lot .

If your budget feels more like a straitjacket than a roadmap, you aren’t the problem. The system is. In 2026, with the cost of living being what it is, we can’t afford to use rigid, old-school budgeting methods that don’t account for real life. At Princevale, we believe a budget should support your life, not control it.

This guide is going to walk you through the exact steps to build a “bulletproof” monthly budget that fits your actual lifestyle, even if your income is tight or as unpredictable as the weather.

Why Most Monthly Budgets Fail (The Brutal Truth)

Before we start building, we have to look at the “rubble” of our past failed attempts. Why is it so hard to stay on track? Usually, it is not a lack of willpower; it’s a lack of reality.

- Underestimating “The Small Stuff”: You budgeted for rent, but forgot that your cat needs premium kibble and you occasionally need to buy a birthday card.

- The “Emergency” Trap: You treat car repairs or annual insurance premiums like “surprises.” Newsflash: they happen every year.

- Budget Burnout: If you try to track every single penny like a forensic accountant, you’ll quit within a week.

- Punishment Mentality: If your budget feels like a “no-fun zone,” your brain will eventually rebel.

A sustainable budget is flexible, honest, and built around your priorities, not your guilt. Let’s change the narrative.

Step 1: Know Your Real Monthly Income

You can’t build a house on shaky ground, and you cannot build a budget on “maybe” money.

If Your Income is Fixed

This is the “easy” version. Look at your paystubs from the last three months. Use your after-tax, take-home pay. Do not budget based on your gross salary; Uncle Sam already took his cut, so don’t count chickens that haven’t hatched.

If Your Income is Irregular (Freelancers & Gig Workers)

This is where most people panic. If you’re a freelancer, a server, or work on commission, your income looks like a mountain range.

- The Fix: Calculate the lowest amount you earned in a single month over the last year. That is your “Floor.” Build your essential budget around that number. Anything you earn above that floor goes straight into savings or towards your “wants” later.

Step 2: List Your Fixed Expenses (The Non-Negotiables)

These are the “I can’t live without these” bills. They usually cost the same every month and have a hard deadline.

- Housing: Rent or mortgage (the big one!).

- Utilities: Power, water, gas. (Tip: Use “Level Billing” if your utility company offers it to keep these costs consistent).

- Connectivity: Phone and internet (In 2026, these are basically human rights).

- Debt: Minimum payments on credit cards or student loans.

Pro-Tip: If these “Fixed” costs are eating up more than 50% of your income, it might be time for a “frugal audit” to see where you can trim the fat.

Step 3: Estimate Variable Expenses Honestly

This is where the wheels usually fall off. Variable expenses change based on your behavior.

Common Variable Categories:

- Groceries: Be honest. Don’t budget $200 if you actually spend $600.

- Transportation: Gas, tolls, or public transit passes.

- Household Supplies: Toilet paper, cleaning products, the stuff you “ran out of” at 9 PM on a Tuesday.

- Dining Out: Yes, include the takeout. If you don’t budget for it, you’ll still do it you’ll just feel bad about it later.

How to get it right: Stop guessing. Open your banking app and look at the last 90 days. Average it out. If you spent $400 on groceries every month for three months, budget $400.

Step 4: Include Sinking Funds (The Secret Sauce)

If you take only one thing away from this guide, let it be this: Sinking Funds are the “Game-Changer.”

A Sinking Fund is just a fancy name for “saving up for a specific, expected expense.” Instead of getting hit with a $600 car registration bill in June, you save $50 a month from January to June.

Examples of Must-Have Sinking Funds:

- Annual Subscriptions: Amazon Prime, Costco, Netflix.

- Holidays & Birthdays: Christmas happens on December 25th every year it should not be a surprise!

- Personal Care: Haircuts, skincare, or that dental cleaning co-pay.

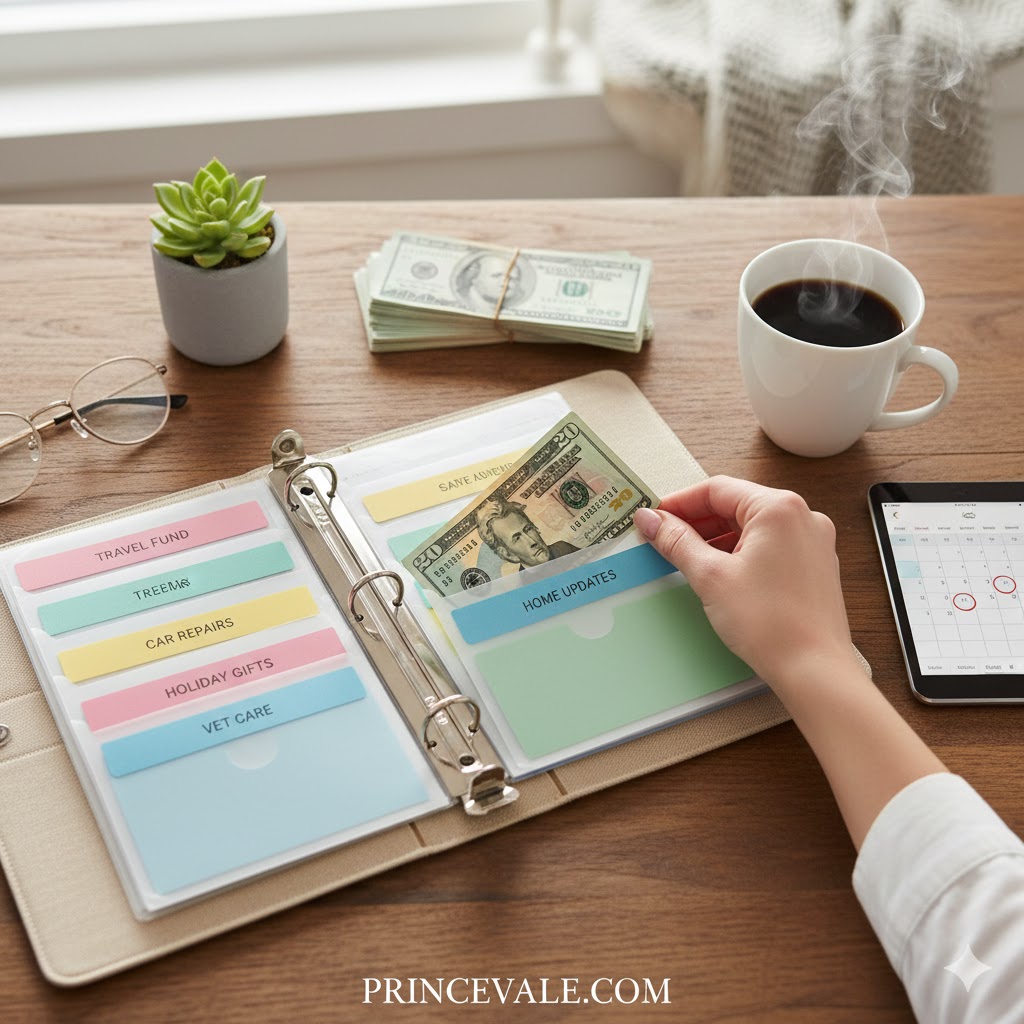

Princevale Resource Recommendation: To keep these funds organized without opening 20 different bank accounts, we love using high-quality [Reusable Cash Envelopes or a Budget Binder] . It’s a physical way to see your money grow for specific goals!

![Reusable Cash Envelopes or a Budget Binder]](https://www.princevale.com/wp-content/uploads/2026/02/Reusable-Cash-Envelopes-or-a-Budget-Binder-1016x1024.jpg)

Step 5: Set a Realistic Savings Goal (Pay Yourself First)

I know, I know. When money is tight, “saving” feels like a luxury. But even $10 a week is a win.

- The Starter Emergency Fund: Aim for $1,000 first. This covers the “life happens” moments a flat tire or a broken microwave.

- The Buffer: Once that’s done, try to build a one-month “cushion” so you’re always spending last month’s money.

Remember: Saving should feel like a victory, not a chore. If you set a goal that’s too high, you’ll fail and give up. Start small and “level up” as you find more frugal wins.

Step 6: Choose a Budgeting System (That Doesn’t Make You Cry)

There is no “perfect” system there is only the system you will actually use.

1. The 50/30/20 Rule

Perfect for beginners. 50% for Needs, 30% for Wants, 20% for Savings/Debt. Simple, clean, effective.

2. Zero-Based Budgeting

Every single dollar has a “job” to do before the month starts. Your Income minus your Expenses should equal exactly zero. This is the ultimate “control” method.

3. The Envelope System

Old school but gold. You put cash in envelopes for categories like “Dining Out.” When the envelope is empty, the party is over.

Budgeting Essential: If you’re a visual person, a [Physical Monthly Budget Planner] is often more effective than an app. There’s something powerful about physically writing down your goals that makes them “stick” in your brain.

![[Physical Monthly Budget Planner]](https://www.princevale.com/wp-content/uploads/2026/02/Physical-Monthly-Budget-Planner-1024x1024.jpg)

Step 7: The “Weekly Check-In” Strategy

Stop trying to track every penny every day. It’s exhausting. Instead, set a “Date Night” with your money once a week (Sunday mornings with coffee are perfect).

During your check-in:

- Review your spending: Did you go over in “Groceries”?

- Adjust: If you overspent on groceries, “steal” $20 from your “Entertainment” category to balance the scales.

- Celebrate: Did you stay under budget in a category? High five yourself!

Step 8: Build in “Life Happens” Flexibility

Rigid budgets break. Flexible budgets last. You must include a Miscellaneous or “Oops” category. This $50–$100 buffer is for the things you forgot—like a school field trip or a sudden craving for Thai food after a long day at work.

If you don’t build in a “Release Valve,” the whole system will explode under pressure.

How Long Does it Actually Take to Stick to a Budget?

Don’t expect to be a pro in 30 days. Most of my readers at Princevale tell me it takes 3 full months to get the hang of it.

- Month 1: You’ll forget half your expenses. It’s okay.

- Month 2: You’ll adjust your numbers.

- Month 3: You’ll finally see your bank balance stop dropping.

Budgeting is a muscle. You’re going to be “sore” at first, but you’re getting stronger every day.

FAQ: How to Create a Monthly Budget

What if I literally don’t have enough money to cover my fixed expenses?

This is a “math problem,” not a “budgeting problem.” You either need to increase your income (side hustle) or drastically reduce your fixed costs (downsizing or negotiating bills). A budget just reveals the truth; it doesn’t create money out of thin air.

Should I pay off debt or save for an emergency first?

In 2026, we recommend the “Hybrid Path.” Save a small $1,000 emergency fund first to stop the cycle of using credit cards for emergencies, then throw every extra penny at your highest-interest debt.

How do I handle “Peer Pressure” spending?

Be honest with your friends! Tell them, “I’m on a strict budget this month to hit a goal.” Suggest a “frugal hangout” like a potluck or a hike instead of an expensive dinner.

Ready to Take Control? (Call to Action)

You don’t have to do this alone! Here are three ways to get started today:

- Join the Community: Follow us on Pinterest for daily “Frugal Living” hacks and Zero-Waste tips.

- Start Your Sinking Funds: Grab your [Budget Binder] today and start saving for the things that matter.

Final Thoughts: It’s About Freedom, Not Restriction

A budget isn’t a wall that keeps you away from your money; it’s a bridge that gets you to your dreams. When your budget reflects your real life, real income, and real priorities, it stops being a burden and starts being a tool for freedom.

Stay consistent, stay kind to yourself, and remember: A small win is still a win.