By Purity Peterson | Princevale | Updated

Quick Summary:Snowball vs Avalanche Debt Payoff Method: Which One Is Right For You? The Snowball Method pays off smallest debts first for fast motivation wins. The Avalanche Method attacks highest interest debt first to save the most money. Both work — the best one is the one YOU will stick to. Keep reading to find out exactly which one that is.

The Debt That Never Seems To End

You know that sinking feeling when you open your bank app and see your debt balance has barely moved — even though you have been making payments faithfully every single month?

You are not lazy. You are not bad with money. You are just using the wrong strategy — or worse, no strategy at all.

Here is the good news: there are two proven methods that have helped millions of people around the world completely eliminate their debt — the Snowball Method and the Avalanche Method.

Both work. Both are free. And one of them is absolutely perfect for your specific situation.

At Princevale we are going to break both down completely — with real numbers, real examples and an honest verdict on which one will actually work best for you.

Let us get into it. 💪

What Exactly Is Debt Anyway?

Before we dive in — let us get honest about what debt really costs you.

Every single debt you carry has two costs:

- 💸 The amount you borrowed — called the principal

- 💸 The interest — the extra money the lender charges you for borrowing

The interest is the sneaky part. It grows every month whether you like it or not. And if you are only making minimum payments — a huge chunk of that payment is going straight to interest, not actually reducing what you owe.

This is exactly why having a deliberate payoff strategy changes everything.

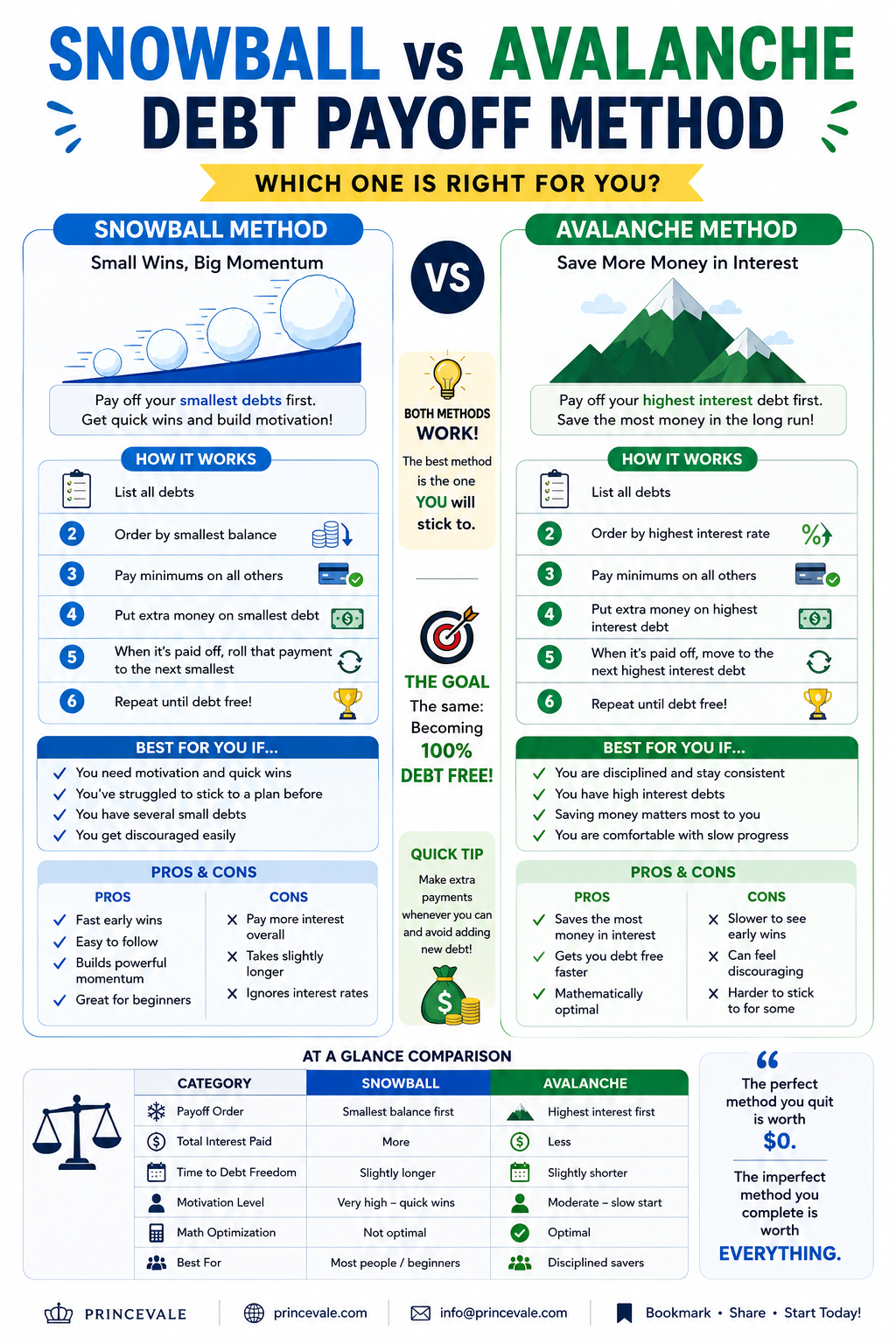

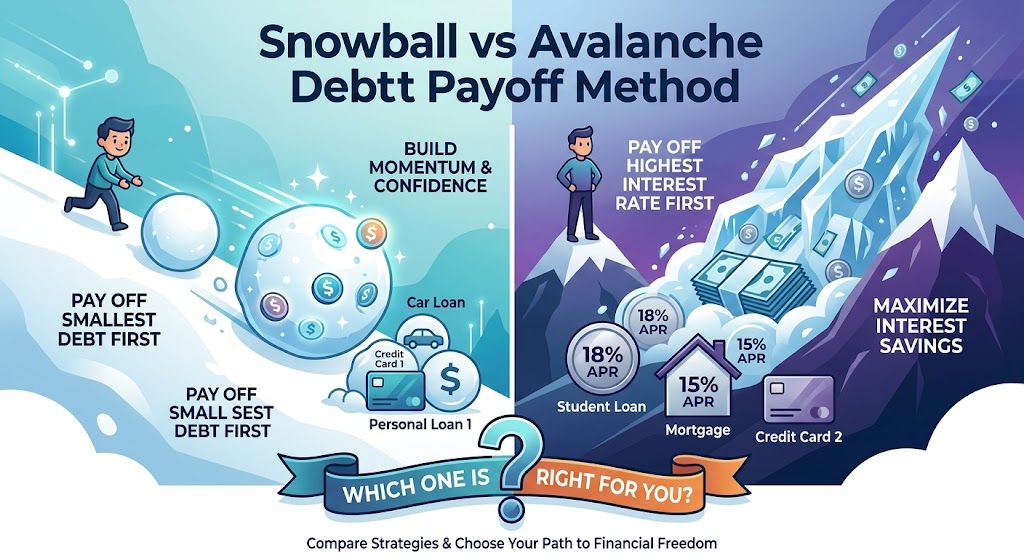

Method 1: The Debt Snowball — Small Wins, Big Momentum

The Debt Snowball Method was made famous by personal finance legend Dave Ramsey and it is built on one beautifully simple idea:

Start small. Win fast. Build unstoppable momentum.

How The Snowball Method Works

| Step | What You Do |

|---|---|

| Step 1 | Write down every single debt you have |

| Step 2 | Order them from smallest balance to largest — ignore interest rates completely |

| Step 3 | Make minimum payments on every debt except the smallest |

| Step 4 | Throw every extra dollar you can find at the smallest debt |

| Step 5 | When it is gone — celebrate properly! You earned it 🎉 |

| Step 6 | Take that payment and add it to the minimum on debt number two |

| Step 7 | Repeat — your payment grows bigger with every debt you kill |

Just like a snowball rolling down a hill — it starts small but gets bigger and faster with every rotation until it is completely unstoppable!

Snowball Method: Real Life Example

Meet Sarah. She has four debts and $300 extra per month to put toward paying them off:

| Debt | Balance | Minimum Payment | Interest Rate | Snowball Order |

|---|---|---|---|---|

| Store credit card | $400 | $25 | 24% | 1st — Attack! |

| Medical bill | $900 | $35 | 0% | 2nd |

| Car loan | $5,200 | $180 | 8% | 3rd |

| Student loan | $14,000 | $220 | 5% | 4th |

Month 1-2: Sarah puts her $300 extra toward the store card ($400). Within 2 months — it is GONE! ✅

Month 3: That $325 ($25 minimum + $300 extra) now rolls into the medical bill attack. The medical bill disappears in about 3 months. ✅

Month 6: Now Sarah has $360 attacking the car loan every month on top of the $180 minimum — totaling $540 per month on that debt alone!

See how the snowball grows? Each victory makes the next one faster and more powerful.

Who Is The Snowball Method Best For?

✅ You have struggled to stick to a debt payoff plan before ✅ You need visible wins to stay motivated ✅ You have several small debts cluttering your budget ✅ You tend to get discouraged when progress feels slow ✅ You are just starting your debt free journey

Snowball Method Pros and Cons

| ✅ Pros | ❌ Cons |

|---|---|

| Fast early wins keep you motivated | You pay more interest overall |

| Simple and easy to follow | Takes slightly longer mathematically |

| Proven to work psychologically | Ignores interest rates completely |

| Builds powerful momentum | May not be optimal for large high interest debts |

| Celebrates progress frequently |

Method 2: The Debt Avalanche — The Math Champion

If the Snowball is about feelings and motivation the Avalanche is about cold hard numbers. It is the strategy a mathematician would choose — and for good reason.

Kill the most expensive debt first. Save the most money overall.

How The Avalanche Method Works

| Step | What You Do |

|---|---|

| Step 1 | Write down every single debt you have |

| Step 2 | Order them from highest interest rate to lowest — ignore balances completely |

| Step 3 | Make minimum payments on every debt except the highest rate one |

| Step 4 | Throw every extra dollar at the highest interest debt |

| Step 5 | When it is gone — move to the next highest interest rate |

| Step 6 | Repeat until every debt is completely eliminated |

Avalanche Method: Real Life Example

Same Sarah. Same four debts. Same $300 extra per month — but now using the Avalanche:

| Debt | Balance | Minimum Payment | Interest Rate | Avalanche Order |

|---|---|---|---|---|

| Store credit card | $400 | $25 | 24% | 1st — Attack! |

| Car loan | $5,200 | $180 | 8% | 2nd |

| Student loan | $14,000 | $220 | 5% | 3rd |

| Medical bill | $900 | $35 | 0% | 4th — Last! |

In this case both methods start with the same debt — the store card — because it happens to be both the smallest AND the highest interest. Lucky coincidence for Sarah!

But watch what happens next:

Snowball Sarah attacks the medical bill ($900 at 0%) next. Avalanche Sarah attacks the car loan ($5,200 at 8%) next.

Avalanche Sarah saves significantly more money in interest because she stops the 8% interest from compounding on $5,200 much sooner. The medical bill at 0% was costing her nothing extra to carry — so attacking it first (Snowball style) would have been pure psychology, not math.

Who Is The Avalanche Method Best For?

✅ You are naturally disciplined and motivated by logic ✅ You have large high interest debts like credit cards ✅ You have tried debt payoff before and know you can stay consistent ✅ Saving money matters more to you than quick wins ✅ You are comfortable with slow steady progress

Avalanche Method Pros and Cons

| ✅ Pros | ❌ Cons |

|---|---|

| Saves the most money in interest | Slower to see early wins |

| Mathematically optimal strategy | Can feel discouraging without quick victories |

| Gets you debt free faster overall | Requires strong self discipline |

| Eliminates most expensive debt first | Harder to stick to for some people |

Snowball vs Avalanche: The Complete Head To Head

| Category | ❄️ Snowball | 🌊 Avalanche |

|---|---|---|

| Payoff order | Smallest balance first | Highest interest first |

| Total interest paid | More | Less |

| Time to debt freedom | Slightly longer | Slightly shorter |

| Motivation level | Very high — quick wins | Moderate — slow start |

| Math optimization | ❌ Not optimal | ✅ Optimal |

| Psychology optimization | ✅ Excellent | ❌ Can be difficult |

| Best for beginners | ✅ Yes | Depends on personality |

| Best for discipline | Works for all | ✅ Best for disciplined |

| Ease of sticking to it | ✅ Easiest | Harder for some |

Which Method Saves More Money? The Honest Numbers

Let us use a simple example with real numbers:

3 debts — $500 extra per month to pay them off:

| Debt | Balance | Interest Rate |

|---|---|---|

| Credit card | $2,000 | 20% |

| Personal loan | $5,000 | 12% |

| Car loan | $8,000 | 6% |

| Method | Total Interest Paid | Time To Debt Free |

|---|---|---|

| Snowball | ~$2,850 | ~28 months |

| Avalanche | ~$2,340 | ~27 months |

| Difference | $510 saved | 1 month faster |

The verdict: The Avalanche saves $510 and one month in this example. Significant — but not life changing. And if the Snowball keeps you motivated enough to actually finish — it wins every single time.

The Most Important Thing Nobody Tells You

Here is the truth that most personal finance articles are too afraid to say clearly:

The perfect method you quit is worth exactly zero dollars. The imperfect method you complete is worth everything.

Research consistently shows that people who experience early wins in a long term challenge are significantly more likely to complete it. This is exactly why Dave Ramsey has helped millions of people become debt free with the Snowball — not because it is mathematically perfect but because it works with human psychology instead of against it.

If you are someone who has started a debt payoff plan before and quit — choose the Snowball. No debate needed.

If you are someone with iron discipline who is motivated by numbers and logic — choose the Avalanche. You will save real money.

The Hybrid Approach — Best of Both Worlds

Can not decide? You do not have to choose just one! Many financial experts recommend a hybrid strategy:

How The Hybrid Works

| Step | Action |

|---|---|

| Step 1 | Pay off any debts under $500 first — fast Snowball wins |

| Step 2 | Switch to pure Avalanche for all remaining debts |

| Step 3 | Get your early motivation boost then maximize your savings |

This gives you the psychological fuel of the Snowball early on and the mathematical efficiency of the Avalanche for the long haul. Many people find this is the perfect balance!

How To Choose — Answer These 5 Questions

Be completely honest with yourself:

| Question | Snowball | Avalanche |

|---|---|---|

| Have I tried paying off debt before and given up? | ✅ Choose Snowball | — |

| Do I need to see progress quickly to stay motivated? | ✅ Choose Snowball | — |

| Am I highly disciplined with money goals? | — | ✅ Choose Avalanche |

| Do I have very large high interest credit card debt? | — | ✅ Choose Avalanche |

| Are most of my debts roughly the same size? | — | ✅ Choose Avalanche |

If you answered yes to the first two — Snowball all the way. If you answered yes to the last three — Avalanche is your winner.

10 Tips To Make Either Method Work Faster

Whichever method you choose these power moves will turbocharge your results:

| # | Tip | Impact |

|---|---|---|

| 1 | Find an extra $100-$200 per month to throw at debt | 🔥 Huge |

| 2 | Cancel unused subscriptions and redirect to debt | ✅ Medium |

| 3 | Start a small side hustle — even $200 extra monthly matters | 🔥 Huge |

| 4 | Use tax refunds and bonuses entirely on debt | 🔥 Huge |

| 5 | Stop adding new debt — cut up credit cards if needed | 🔥 Critical |

| 6 | Build a small $1000 emergency fund first | ✅ Essential |

| 7 | Track your progress visually — a chart on your wall works | ✅ Motivating |

| 8 | Tell someone your goal — accountability is powerful | ✅ Medium |

| 9 | Celebrate every single payoff — even small ones | ✅ Motivating |

| 10 | Automate your extra payment so you never forget | 🔥 Huge |

7 Mistakes That Will Derail Your Debt Payoff

Avoid these at all costs:

| ❌ Mistake | 💥 Why It Destroys Your Progress |

|---|---|

| Continuing to use credit cards while paying off debt | Filling a bucket with a hole in it |

| Having no emergency fund | One car repair sends you back into debt |

| Only making minimum payments | Interest eats your payments alive |

| Trying to pay off debt without a budget | You have no idea where your money is going |

| Quitting after one bad month | Progress is never perfectly linear |

| Comparing your journey to others | Everyone’s debt story is different |

| Not celebrating your wins | Motivation dies without acknowledgment |

Real People, Real Results

Sarah’s Snowball Story

“I had 6 debts and felt completely overwhelmed. I tried the Avalanche first but after 4 months of barely seeing progress I gave up. Then I switched to the Snowball. I paid off my first debt in 6 weeks and cried actual tears. That feeling kept me going. 18 months later I was completely debt free.”

Michael’s Avalanche Victory

“I am an accountant so the math made the decision for me. I had $28,000 in credit card debt at 22% interest. Every month I delayed was costing me real money. The Avalanche saved me over $3,000 in interest compared to the Snowball. Numbers do not lie.”

Both methods work. Both people won. The method matched the person , and that made all the difference.

Your Debt Free Action Plan — Start Today

Do not let this article be something you read and forget. Take action right now:

| ✅ Action | When |

|---|---|

| Write down every single debt you have with balances and interest rates | Today |

| Choose your method — Snowball, Avalanche or Hybrid | Today |

| Calculate your extra monthly payment amount | Today |

| Set up automatic payments | This week |

| Download our free debt payoff tracker | Right now below ⬇️ |

| Tell one person your debt free goal | Today |

Free Resource — Your Debt Payoff Tracker 🎁

To help you get started we have created a free printable debt payoff tracker you can download and stick on your wall — because seeing your progress every single day is one of the most powerful motivators there is.

👉 [Download Your Free Debt Payoff Tracker Here]

The Bottom Line

| ❄️ Snowball | 🌊 Avalanche | |

|---|---|---|

| Choose if | You need motivation and quick wins | You are disciplined and want to save money |

| Best feature | Psychological momentum | Mathematical optimization |

| Our rating | ⭐⭐⭐⭐⭐ for most people | ⭐⭐⭐⭐⭐ for disciplined savers |

Both the Snowball and Avalanche methods are proven, powerful and completely free to use. The only wrong choice is choosing neither and continuing to let debt control your life.

Your debt free journey starts with one decision. Make it today. 💚

At Princevale we believe that smart spending starts with a smart plan. Whether you are just starting out or ready to finally finish what you started — we are here to walk every step of this journey with you.

📌 Bookmark this article — share it with someone who needs it 🌐 Visit us: princevale.com 📧 Email us: https://www.princevale.com/

Conclusion: Snowball vs Avalanche Debt Payoff Method

Debt can feel like a heavy weight you carry everywhere you go to work, to bed, to every family dinner and every holiday celebration. It whispers that you will never get ahead. That you will always be one unexpected bill away from disaster. That financial freedom is for other people not you.

But here is what we want you to walk away knowing today:

You now have two of the most powerful debt elimination strategies in the world sitting right in your hands completely free.

Whether you choose the Snowball Method with its fast motivating wins or the Avalanche Method with its mathematically superior savings you are no longer guessing. You are no longer stuck. You have a plan.

And a plan even an imperfect one changes everything.